doing real estate differently

Buyers

Preparation is Key

Understanding the process will make you a stronger, more confident buyer and better negotiator.

-

Know your buying power

Before viewing homes, you should know what you want to spend and how much you should spend. Speak with a lender to get your pre-approval letter and to discuss the following:

Purchase Price

Lender Fees

Closing Fees

Downpayment

Monthly Payments (PITI: Principal, Interest, Taxes, Insurance plus potential PMI: Private Mortgage Insurance)

Do you have a house-sale contingency? (Need to sell a house to qualify for a loan.)

Are you actually a cash buyer and not getting a loan?

Do you quality for Conventional, FHA, VA financing or something else?

Do you need gift money from a family member?

-

Before viewing homes, we will sit down together to discuss

Your real estate goals

The Buying Process

Who real estate agents represent

The services real estate agents provide

How real estate brokers and agents get compensated

Buyer consultations and Buyer Broker Agreements are not optional. They are a step required by the National Association of Realtors and are Ohio law.

-

There are Strategies for making offers, and even more strategies when you’re up against multiple buyer offers. The following breaks down the financial considerations before and during the transaction.

All offers differ. Here are some typical Elements of an Offer:

Purchase Price

Closing Costs

Buyer Agent Commission

Earnest Money

Home Warranty

Inspection Costs

Potential Repairs/Reno Costs

Appraisal Fee

Appraisal Gap

What does it really cost to buy a home?

Let’s break it down using $100,000 as an example purchase price.

The following rates and percentages vary. This is only an example.

1. What’s Due At Closing

Purchase Price: $100,000

Down Payment (10%): $10,000

Loan Amount: $90,000

Estimated Closing Costs (3%): $3,000

Buyer Agent Commission (3%): $3,000

(Typically paid by the seller)

Estimated total due from buyer at Closing: $16,000

2. What You’ll Pay During the Transaction

These are expenses that happen before closing.

Earnest Money: Usually between $1,000 and 1% of purchase price.

(Held by title company and credited to your closing costs)

Inspections: $350-$1,000 | Let’s say $500

The amount will vary, depending on how many you choose.

Appraisal Fee: $500–$700 | Let’s say $500

Your lender may require this upfront or include it in closing costs.

Estimated total due from buyer during transaction,

Prior to Closing: $2,000

3. Possible Additional Costs

Not every transaction includes these, but it’s smart to understand them.

Inspection Repairs:

Many inspection reports indicate needed repairs. Let's say $2,000–$10,000 is recommended.

Can you afford this?

Try to negotiate repairs or credits with the seller may reduce your responsibility.

Appraisal Gap:

If the home appraises lower than your offer, you may need to pay the difference out-of-pocket.

Example:

Appraised at $95,000

You offered $100,000

You may owe $5,000 out-of-pocket.

You can also try to negotiate the purchase price again here!

Home Waranty:

Optional: ~$500 for 1-year coverage on appliances & systems.

If seller doesn’t provide one, you can buy it yourself.

4. Example Scenario: How the Numbers Shift

Let’s say:

$16,000 originally due at closing

- BUT -

$1,000 earnest money already paid

$3,000 Seller covers your commission

$1,500 Seller contributes toward closing costs

Adjusted Total Due at Closing: $10,500

Now let’s say:

$2,000 needed for appraisal gap

$500 home warranty added

Final Adjusted Closing Amount: $13,000

AND how much total out-of-pocket would you spend in this scenario?

$13,000 at closing plus your $2,000 during the transaction

Grand Total: $15,000

Typical 30-Day Real Estate Transaction

The following is an example of a typical real estate transaction. Day 1 begins when both buyer and seller have signed the Residential Purchase Agreement. Day 30 is the final day when the home is officially sold and the buyer becomes the owner. Dates, tasks, and events of your transaction may differ.

DAY 1-5

Earnest Money Deposited

Written Loan Application

DAY 1-10

Removal of Contingencies

Negotiate repairs

DAY 30

Buyer & seller sign final documents with title company

Buyer wires money for purchase of property

DAY 10-20

Appraiser visits property to determine its value

DAY 27-29

Buyer visits property to be sure there is no new damage

DAY 25-28

Buyer and seller call utility companies to set up transfer date

DAY 20-27

Buyer obtains a Written Loan Commitment from lender

DAY 30-31

Seller gets paid

Buyer now owns property and gets keys

Congratulations!

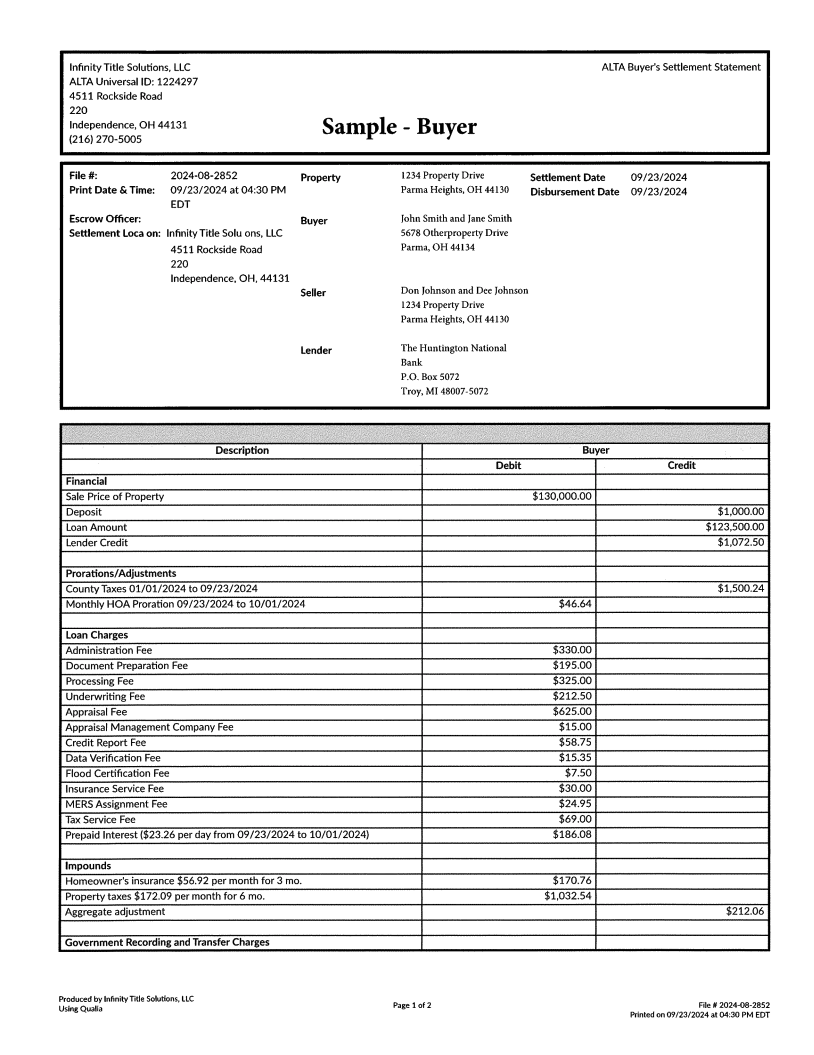

Buyer’s ALTA Settlement Statement

Prior to signing all your closing documents with the title company, the lender will send you a Closing Disclosure. The title company will balance lender fees with title fees to complete the finalized ALTA (American Land Title Association) Settlement Statement. This is a line-by-line breakdown of your costs (purchase price, lender closing costs, title/escrow fees, title insurance, pre-paid taxes & insurance, etc.) due at closing.

Purchase Price

Closing Costs

Escrow Fees

Title Insurance

Prepaid Taxes and Insurance

It ensures transparency before closing. We’ll review this together so you understand every item.

Client for Life

After all the i’s are dotted and t’s are crossed, and you’re all moved in, I’m still here for you. Always feel welcome to ask about home warranties, contractor recommendations, and to send me referrals. I look forward to helping you, your family, and friends for years to come!